AI saving strategies to build your emergency fund fast in 2026. Smart tools, real tips, and actionable steps to secure your finances today.

How to Build an Emergency Fund Fast Using AI Saving Strategies

Three years ago, my car broke down on a Tuesday morning and I had exactly $47 in my bank account. No emergency fund. No backup plan. Just a sinking feeling in my stomach that I had been one unexpected bill away from disaster for years without even realizing it.

That moment changed how I thought about money permanently. AI Saving Strategies

What changed my actual financial behavior, though, was discovering AI saving strategies that took the guesswork, the guilt, and the friction almost completely out of the process. Within eight months I had a fully funded three-month emergency fund. Not because I suddenly earned more. Because I finally had the right tools working for me in the background every single day.

If you are starting from zero or feel like saving feels impossible on your current income, this article is written specifically for you. The strategies here are practical, proven, and powered by technology that does most of the heavy lifting so you do not have to.

Why Most People Never Build an Emergency Fund and How AI Changes That

The standard financial advice is painfully simple. Spend less than you earn and save the difference. If that advice actually worked reliably, most households would not be one car repair away from financial stress.

The problem is not knowledge. It is behavior, consistency, and visibility.

People fail to build emergency funds for three consistent reasons. First, they have no clear picture of how much they can actually save each month without affecting their lifestyle in ways that feel unsustainable. Second, saving requires an active decision every pay period, and active decisions are vulnerable to bad moods, unexpected expenses, and simple forgetfulness. Third, the timeline feels so long that motivation fades before the habit forms.

AI saving strategies address all three of these problems simultaneously, which is why they produce results that willpower-based approaches rarely sustain.

What AI Saving Strategies Actually Mean in Practice

This is worth clarifying because the phrase can sound more futuristic or complicated than it actually is.

AI saving strategies are not about robots managing your investment portfolio or algorithms making complex financial decisions on your behalf. At the everyday level, they refer to using machine learning-powered tools to analyze your income and spending patterns, identify genuine saving opportunities, automate transfers at optimal times, and adjust your saving behavior based on real data about how your money moves.

The core advantage is personalization at scale. A human financial advisor can give you a savings plan based on a one-hour conversation. An AI tool can give you a savings plan based on 18 months of your actual transaction history, updated daily, and refined continuously as your situation changes.

That depth of insight, delivered for free or near-free, is genuinely new. And it works.

How to Build Your Emergency Fund Fast Using AI Saving Strategies

Step One — Know Your Actual Target Before You Start Saving

Most financial advice says save three to six months of expenses for your emergency fund. That range is so wide it is almost useless without personalization.

Before you save a single dollar, use an AI budgeting tool like Copilot, Monarch Money, or YNAB to pull your last three months of spending data and calculate your true monthly essential expenses. This means rent or mortgage, utilities, groceries, transportation, insurance, and minimum debt payments. Nothing discretionary.

For most people, this number is significantly lower than their total monthly spending. Knowing your real target — say, $6,400 instead of a vague “six months of salary” — makes the goal feel achievable and gives the AI a concrete number to build a plan around.

This step alone changes the psychological relationship most people have with the goal.

Step Two — Use AI to Find the Money You Did Not Know You Had

Here is where AI saving strategies genuinely earn their reputation.

Apps like PocketGuard and Cleo analyze your spending automatically and surface waste you are too close to your own finances to see clearly. Forgotten subscriptions, inflated utility bills, spending category creep, seasonal patterns that drain your account in predictable ways — the AI sees all of it.

In practice, this step tends to find between $100 and $400 per month for the average household. That is money already leaving your account that could be redirected entirely to your emergency fund with zero change to your actual quality of life.

One user I know discovered she was paying for three different music streaming services simultaneously — a combined $42 per month she had never consciously decided to spend. Canceling two of them and redirecting that money added $504 to her emergency fund in the first year without her feeling any difference in her daily life.

Multiply that logic across subscriptions, bill negotiation, and optimized grocery spending, and the savings potential becomes substantial very quickly.

Step Three — Automate Everything Using Intelligent Micro-Saving

Manual saving is the single biggest obstacle to actually building an emergency fund. If saving requires you to make a conscious decision every pay period, life will eventually get in the way.

The solution is automation, and AI-powered tools have made this smarter than ever.

Apps like Digit and Chime use AI algorithms to analyze your checking account balance, your upcoming bills, and your income schedule and then automatically transfer small amounts — sometimes as little as $2 or $3 — into a separate savings account on days when you can genuinely afford it.

The genius of this approach is that the transfers are invisible. They never happen in amounts large enough to cause stress or trigger a decision to override them. But they add up consistently over time in a way that feels almost passive.

Digit users save an average of $2,500 in their first year without actively budgeting, according to the company’s reported data. For someone building an emergency fund from zero, that figure can represent meaningful progress without any dramatic change in behavior.

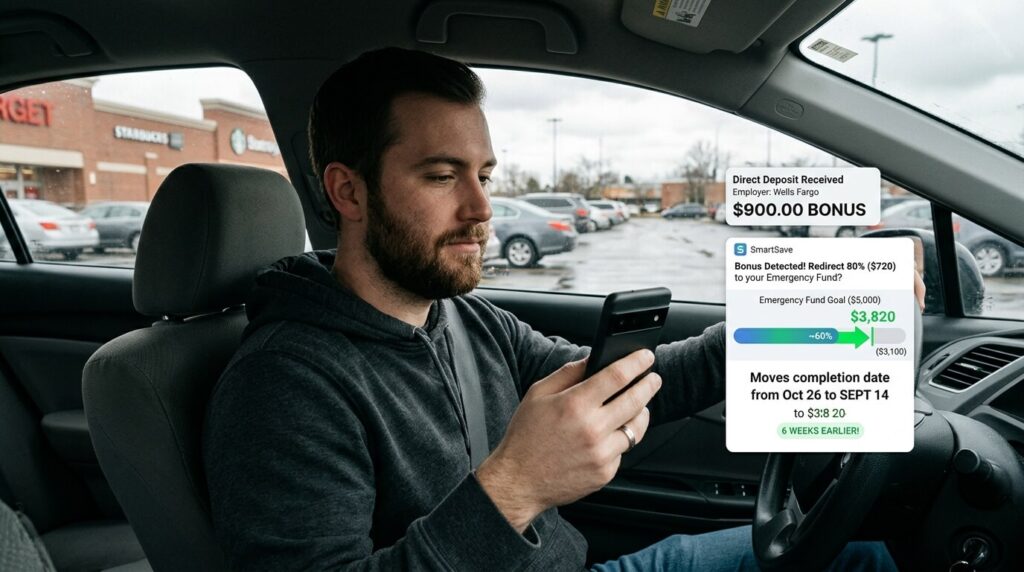

Step Four — Apply the Round-Up and Windfall Strategy

Most major banks and fintech apps now offer a round-up feature powered by AI. Every time you spend — say $4.60 on a coffee — the app rounds up to the nearest dollar and transfers the $0.40 difference to your savings automatically.

This sounds trivial. Over a month of normal spending, most people generate between $30 and $65 in round-ups. That is $360 to $780 per year added to an emergency fund without a single intentional saving decision.

Pair this with a windfall rule — directing 50 to 80 percent of any unexpected money directly to your emergency fund — and the growth accelerates noticeably. Tax refunds, freelance income, birthday money, work bonuses. The AI tools make it easy to set this rule once and have it execute automatically every time money arrives outside your regular paycheck.

Step Five — Use AI Goal Tracking to Stay Motivated Long Enough to Finish

This step is underestimated by almost everyone.

The behavioral research on saving is consistent. People who can see their progress toward a specific, visualized goal save faster and sustain the behavior longer than people saving toward a vague target. AI budgeting apps have made goal visualization genuinely compelling.

Monarch Money and YNAB both offer goal tracking that shows your emergency fund progress in real time, projects your completion date based on current behavior, and notifies you when you are ahead of schedule or falling behind. Some apps adjust the projection daily as your spending changes.

Watching a progress bar move toward a goal you genuinely care about is a more powerful motivator than most people expect until they experience it. Set the goal inside the app with a real target date and let the visual accountability do its work.

Real-World Example — From Zero to Fully Funded in Seven Months

A freelance graphic designer earning approximately $3,200 per month after taxes combined four AI saving strategies simultaneously over seven months.

She used Copilot to identify her true monthly essential expenses, which came to $2,100. That set her emergency fund target at $6,300 for three months of coverage. She used PocketGuard to cancel $170 in unused or duplicated subscriptions. She enabled round-ups through her bank app and set up Digit for automated micro-saving. She redirected two client project bonuses totaling $900 directly to her emergency fund using a windfall rule she had pre-set in her budgeting app.

Seven months later she had $6,450 saved. She had not changed her freelance rates, taken a second job, or made dramatic lifestyle cuts. She had simply let four AI tools work simultaneously in the background while she focused on her actual work.

That is what a coordinated AI saving strategy looks like in practice.

Expert Tips to Accelerate Your Emergency Fund Growth

Open a dedicated high-yield savings account separate from your everyday checking account. The psychological separation matters enormously. When emergency fund money sits alongside spending money, the boundary erodes. Many AI budgeting apps integrate directly with high-yield savings accounts, making the connection seamless.

Set your emergency fund as the single financial priority for 90 days. Not investment contributions. Not extra debt payments beyond minimums. Just the emergency fund. A focused 90-day sprint builds momentum that makes every subsequent financial goal easier.

Tell the AI your goal in specific terms. Apps like YNAB and Monarch Money allow you to input a named goal with a target amount and a deadline. The specificity improves the quality of the AI recommendations and gives you a concrete milestone to work toward.

Review the AI recommendations weekly, not daily. Daily review creates anxiety. Weekly review creates adjustment. Set a 15-minute weekly money check-in where you look at your progress, review any new AI suggestions, and make any necessary course corrections.

Do not pause saving during difficult months. This is where most people break the habit. When a tough month arrives, reduce the automated transfer amount instead of stopping it entirely. Even saving $20 in a hard month preserves the habit and the momentum.

FAQ Section

What is the fastest way to build an emergency fund using AI saving strategies?

The fastest approach combines four methods simultaneously. Use an AI budgeting app to identify and eliminate wasted spending, enable automated micro-saving through a tool like Digit or Chime, activate round-up saving on all your purchases, and apply a windfall rule that redirects unexpected income directly to your emergency fund. Together these methods can accelerate fund growth significantly without requiring dramatic lifestyle changes.

How much should my emergency fund actually be?

The standard recommendation is three to six months of essential living expenses, not total income. Use an AI budgeting app to calculate your true monthly essential costs — rent, utilities, groceries, transportation, insurance, and minimum debt payments — and multiply by three for a starter fund and by six for a comprehensive one. Most people find their essential expenses are considerably lower than their total spending.

Can AI saving strategies work if I have a low income?

Yes, and in some ways they work better on tight budgets because the optimization matters more. Micro-saving tools like Digit work in very small increments, round-ups function regardless of income level, and the subscription and bill identification features tend to find proportionally significant savings for people spending carefully. Start with whatever amount the AI recommends as your safe-to-save figure, even if it is small.

Which AI saving app is best for beginners building their first emergency fund?

PocketGuard is the most accessible starting point because it reduces your entire financial picture to a single daily number showing exactly how much you can safely spend. YNAB is the most effective for people ready to engage more actively with their finances. Digit is ideal for anyone who wants fully automated saving with minimal ongoing involvement.

How long does it realistically take to build a three-month emergency fund?

Timeline depends entirely on income, expenses, and how aggressively the AI strategies are applied. Based on typical results reported by users of major AI budgeting apps, most people building from zero can reach a three-month emergency fund within six to twelve months when combining automated saving with identified spending optimization. Some complete it faster when windfalls are redirected effectively.

Is it safe to connect my bank account to AI saving apps?

Reputable AI saving apps use bank-level 256-bit encryption and connect through read-only access, meaning they can analyze your transactions but cannot initiate unauthorized transfers or access your funds directly. Stick to established platforms like Digit, YNAB, Copilot, and Monarch Money, and review each app’s privacy policy before connecting your accounts.

What should I do once my emergency fund is fully funded?

Once you reach your three to six month target, redirect the automated saving contributions toward your next financial goal — typically high-interest debt elimination or retirement contributions. Keep the emergency fund in a high-yield savings account where it earns interest and remains accessible. Do not invest it in anything that could lose value or require time to liquidate, as its entire purpose is instant accessibility during genuine emergencies.

Internal Linking Suggestions

An article titled “/chatgpt-vs-claude-for-marketing/

A piece on “/ai-tools-for-small-business/

A roundup titled “/email-marketing/

External Authority Source Suggestions

The Federal Reserve’s Report on the Economic Well-Being of US Households at federalreserve.gov provides authoritative data on emergency fund statistics and American savings rates, adding immediate credibility to claims about how many households are financially vulnerable.

Conclusion

The car breakdown that left me with $47 in my account was one of the most clarifying moments of my financial life. Not because it was dramatic, but because it revealed exactly how exposed I had been living without ever acknowledging it.

The difference between then and now is not income. It is systems. Specifically, AI saving strategies that do the analysis, the automation, and the behavioral nudging that I was never disciplined enough to sustain on my own.

An emergency fund is not a luxury for people who already have money figured out. It is the foundation that makes everything else in your financial life possible. With debt. With career risk. With health. With relationships. Every area of your life gets less stressful when you know that a single unexpected expense cannot unravel everything.

The tools to build that foundation are free, accessible, and smarter than they have ever been. The only thing left is to start.

Open one app today. Connect your account. Let the AI show you what is actually happening with your money. Then follow its first recommendation, whatever that turns out to be.

The version of you with a fully funded emergency fund is closer than you think, and the path there is more manageable than it has ever been.