Emergency fund how much should I save? Learn exactly how much money to set aside, how to calculate your target, and build lasting financial security

Emergency Fund: What’s my savings amount ?

Many people are faced with unexpected expenses. Emergency events such as loss of employment or a major medical expense (or both), sudden and necessary home or vehicle repairs can quickly compromise your financial situation if you have not taken the time to create a sound emergency fund.

Emergency Fund is actually a very important thing that you should take to achieve financial stability. However, a lot of people simply continue to ask the same question over again: What amount should I place in my Emergency Fund?

It actually depends on basically two aspects of your personal circumstances, i.e. on your level of income and your amount of expense, as well as your job security. There are not really set numbers that work for everyone, but there are some time-tested rules that will help you figure out what number works best for you.

As you will see from this guide, you will know the amount of money you should keep in an emergency savings account, how to calculate your ideal amount of savings, the common mistakes made by many individuals, and the practical strategies that will accelerate your efforts to meet your savings goal.

Description of Emergency Fund

An emergency fund is money that is set aside for a specific role – to cover unexpected expenses or financial emergencies. Unlike savings that are intended for vacations, shopping, or planned purchases, the only time emergency savings (funds) should be used is when you are experiencing a true financial hardship. Types of Events for which to Use Emergency Funds:

Unexpected Expenses (Medical )

Job loss or Reduction of Income

large Expenses (Car Repairs)

large Expenses (Home Repairs)

Family Emergencies

Urgent Travel

The emergency fund will protect you financially during life will turn unpredictable.

How Much Should I Have in my Emergency Fund?

Most financial experts will recommend that you save

Situation Recommended Emergency Fund

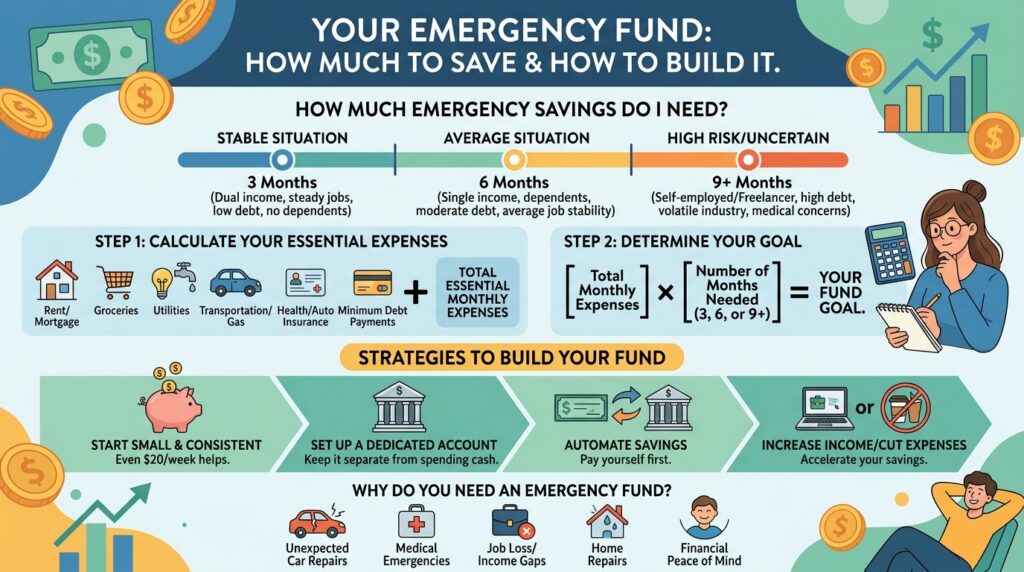

Safe income and minimal risk: three months worth of essential expenses.

A moderate amount of financial uncertainty is typically covered by three to six months of expenses.

Freelancers and/or business owners should keep 6–12 months’ expenses in reserve.

Households that have only one source of income should have an emergency fund equal to at least 6–12 months of living expenses saved.

What’s appropriate for a household may vary slightly based on the individual’s or households’ actual financial condition and not necessarily an established amount of money.

A reasonable amount of money in an emergency fund would be between 3-6 months worth of living expense for the average person. For individuals with irregular income (e.g. freelancers, contractors) or self-employed or those who are at higher risk of incurring large expenses due to an emergency situation will benefit from trying to save between 6-12 months worth of expenses for increased protection.

Reason behind the Most and Popular Opinion, The Three to Six Months”

Emergencies generally occur at totally inopportune moments.

If you have lost your job, it may take several months before you find another one. That is when your emergency fund can come in handy to help pay your housing expenses, utilities, food, insurance, transportation, and minimum debt payments.

Being in possession of several months’ worth of living expenses will help ease your financial burden associated with an emergency situation and protect you from having to borrow money via a credit card or loan.

How to calculate emergency fund goals

First, start with listing out all of your basic monthly expenses. Now, just look at the things you ‘have to have’. Here is a list of some common basic needs you may have:

. Rent/mortgage

. Utilities

. Groceries

. Insurance

. Transportation

. Medical expenses

. Minimum debt payments

Assume these are the monthly basic needs:

Expense Monthly Amount

Rent $800

Electricity $150

Groceries $300

Transportation $150

Insurance $100

Debt Payments $200

Total $1,700

The next step is to multiply by the amount of months you want to cover in your Emergency Fund. So:

3 months: $1,700 x 3 = $5,100

6 months: $1,700 x 6 = $10,200

12 months: $1,700 x 12 = $20,400

So now you are armed with a realistic savings target based on your way of life.

Factors That Determine the Amount of Savings You Need to Have

The Stability of Your Job

A person with a stable job will need less of an emergency fund than those who have unstable jobs. Consider the following factors: (a) the probability of being laid off, (b) your industry demand, (c) your industry economic climate, (d) your employment contract (ie: are you employed on a permanent basis / on contract), (e) your income consistency and position within the organization (ie; are you a freelancer, consultant or business owner and have fluctuating income).

While monthly income may vary, therefore additional funds in your emergency fund provide additional safety to you when there is an emergency situation.

number of dependents: When you support any family members or children, your financial responsibility will also increase, therefore you should higher savings target, more funds to cover expenses and more financial flexibilities for your dependents.

Health related matters:

Those who are subject to higher healthcare costs should have larger amounts of cash set aside for their unexpected medical expenses.

Emergency Savings Goals By Financial Stage

Starter Goal – $1000.

For a brand new person, just try to get the first $1000 together.

$1000 can cover lots of typical emergencies (things like car repair, a new appliance, small medical bill).

After reaching the $1000, you will feel much more motivated and confident to keep saving.

Intermediate Goal -3 Months of Expenses

Once you reach a starter fund, work on increasing it so that it will cover your family’s essential expenses for three months.

You can get a good amount of protection for a short time of financial issues.

Long-Term Emergency Fund (Six to Twelve Months)

Large Emergency Fund will work for the following categories:

Self-Employed People,

Owners of Businesses,

Families with only one source of income, and/or

Individuals working in unstable industries.

It gives you the most resilience against financial difficulties.

Emergency Fund Storage Areas

In determining where to keep your emergency fund, accessibility is a major consideration.

The ideal characteristics of an emergency fund include:

Access (Easy),

Apart from everyday spending accounts,

and

Not subject to the volatility of the stock market.

The most accessible options for storing your emergency fund includes:

Option

Advantage

Disadvantage

High-Yield Savings Account

Accessible + earns interest

Lower rate of return compared with investments

Money Market Account

Accessible + safe

Limited growth potential

Cash Management Account

Easy to access

Interest rates are variable

In other words, so avoid using your “rainy day” money to invest in stocks or any high-risk asset because a market downturn could happen, which would reduce your available funds when you really need them.

Common Mistakes Made With Emergency Funds

Saving too small an amount.

Another disadvantage of having a small emergency fund is that a major job loss or other unexpected expense might go uncovered by your current funds.

Saving too much.

A lot of cash in an emergency fund reduces the amount of long term money you need to grow your wealth. You can put your money to better use by continuing to save once you have reached your goal and using that money for investments, saving for retirement, or paying off debt.

Spending your emergency fund for non-emergencies.

For example, vacations, or shopping or entertainment purchases are not emergencies. You should only spend this money on true emergencies.

Having your money too easily accessible to yourself.

If your emergency fund is combined with your daily money, it will make it more difficult for you not to spend it. You might want to keep your emergency fund in a separate bank account.

Useful Tools to make your emergency fund grow faster

Automate Savings

Set up automatic payments from each pay check.

You do not have to think about making a decision every time you want to put money into your savings account.

Save Unexpected Money

You may want to consider putting all or part of any unexpected money (such as:

Bonuses Tax Refunds Gifts Side Income)

toward your savings account. They can help you reach your goal much faster too.

Reduce Non-Essential Spending (the “Wants”)

Analyze all of your non-essential monthly subscriptions and purchases. Although it may not seem like much, cutting back here and there can really add up quickly!

Earn Additional Income

Emergency fund contributions can also come from temporary work (side gigs or freelance work), as well as selling things you no longer need.

Pros & Cons of Having a Large Emergency Fund

Pros – Creates a greater sense of financial security, Reduces your stress associated with your finances, Allows you to rely less on credit cards or loans to pay off debt and provides you with an additional cushion in case you were to become unemployed.

Cons – Reduces investment growth potential, You will incur an “opportunity cost” from holding the funds as cash, Inflation will erode your purchasing power over time, And, it will take time and discipline to build the emergency fund. For most individuals creating an emergency fund provides a much greater level of financial security than the negatives associated with maintaining that emergency fund.

Best Practises for the Emergency Fund.

Check it often

As your expenses go up so should the amount you try to save.

Rebuild after you use it.

If you use money from your fund for an emergency, work to rebuild it.

Change how much you have in savings if your life changes a lot (like marriage, having a baby, moving, getting a new job etc).

FAQs

Is $1,000 a good emergency fund?

$1,000 is a good starting point for an emergency fund, but most people will need to save enough money to pay for living expenses for a few months.

Should I pay off my debt before saving for emergencies?

In most situations, creating a minor emergency fund before making every effort to pay off your debts provides a protective cushion for you to rely on for covering unexpected expenses and avoids further borrowing.

Is it right to invest my Emergency Fund?

Therefore, the money should be held in very secure, liquid accounts and not in volatile investment types. At emergency fund, you should favour availability and stability of your money as opposed to obtaining a high return.

Conclusion

Emergency fund how much should I save? is a basic question to answer with two simple numbers; 1. what are your monthly essential expenses, and 2. what is your personal financial risk.

An emergency fund amount of three to six months expenses will provide a solid foundation for most people. If you have a variable income or dependents or face significantly more uncertainty, you may benefit from saving six to twelve months of expenses in your fund.

Getting started as soon as possible is vital and the numbers don’t even really matter. Even having a semi-functional emergency fund can shield you from financial hurdles, ease the strain emotionally, as well as loan you greater command over your future.

Consistently contribute, use automation when able, and look at your emergency fund for what it truly is- a long-term protective cushion against unexpected expenses. Over the years, that cushion could end up being a major holding in your finances.